The Yellow Table

25 April 2008

Revenues for the world's 50 largest construction equipment manufacturers totalled US$ 98.8 billion last year, a +14.4% increase on the previous year's total of US$ 86.3 billion. This year is the fourth time IC has compiled the Yellow Table, and that period has seen sales for the top 50 grow continuously from US$ 55.5 billion in the 2003 edition (based on 2002 sales) – an overall increase of +78% over four years.

Regular readers of IC may remember that last year's Yellow Table saw a massive sales increase of +31.1% from the 2004 edition. So while this year's growth figure of +14.4% is positive for the industry, it could also be a sign that a down turn is approaching.

Top Cat

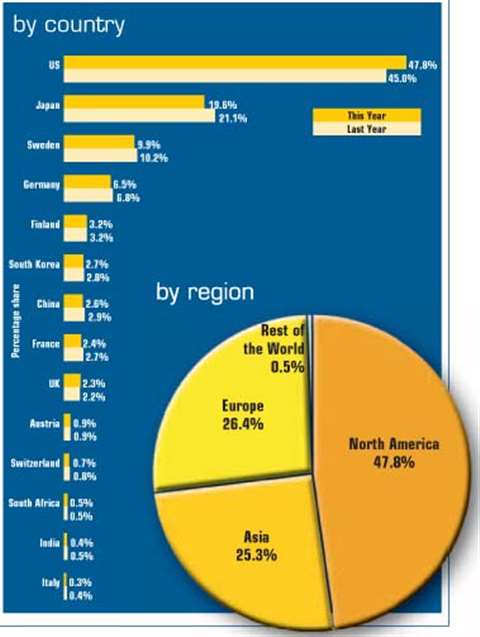

Caterpillar of course leads the Yellow Table by a wide and growing margin. Based on 2005 annual results it accounted for 23.2% of the top 50 manufacturers' sales – an increase of +1.6 percentage points from its 21.7% share of last year's Yellow Table. Komatsu is once again in second place, with an unchanged 9.6% portion, and Terex retains third place with 6.5%, an increase of +0.7 percentage points from last year.

The improved shares that Caterpillar and Terex have achieved reflect a strong performance for all the US manufacturers. All have at least maintained their positions from last year, while many improved their standing. The only exception is Altec Industries, which slipped six places due to IC revising its estimate for the company's sales.

But aside from this, US manufacturers have made some significant moves up the Yellow Table. John Deere has overtaken Volvo to claim fourth place, while both JLG and Manitowoc have moved into the top 15 for the first time. Further down, Astec and Gehl also improved their positions.

US manufacturers accounted for 47.8% of sales of the 50 Yellow Table companies – an increase of +2.8 percentage points from last year's figure of 45%. Going back another year, US manufacturers had a share of 43.4%, which underlines the increasing 'slice' of global construction equipment sales they are capturing. This +4.4 point rise over the last 2 years is equivalent to US$ 4.35 billion per year, based on 2005 figures.

Last year's edition of the Yellow Table showed that both North American and Asian manufacturers had grown their market shares at the expense of the Europeans. However, this year the Europeans have held their ground better, with the US companies' gains coming largely at the expense of the Asian construction equipment manufacturers.

It is always dangerous to make predictions, but it seems likely that this year will see a resurgence for the Asian manufacturers.

Admittedly Europe's slice of the market this year is 26.3%, -0.6 percentage points lower than last year's total of 26.9%. However, the Asian manufacturers' share has slipped -2.5 points to 25.4%.

Looking down the Yellow Table, it is easy to pick out the symptoms of this overall trend. In the top 10 Liebherr has overtaken Hitachi, while other Asian manufacturers dropping down the table include Kobelco, Doosan, Sumitomo and Kato.

Japanese manufacturers make up the biggest block of Asian construction equipment companies, so naturally this year's Yellow Table reflects a noticeable drop in Japan's share of the industry. With a total slice of 19.6%, this is the lowest share Japanese manufacturers have had in the Yellow Table's four-year history.

The Chinese manufacturers also saw their share of the world market slide last year, from 2.9% to 2.6%. Most of the leading players, including Liugong, Sany, Shandong Heungkong, Xaimen and XCMG lost places, and last year's 50th placed manufacturer, Shantui, dropped off the bottom of the Yellow Table.

Only Zoomlion moved up the Yellow Table, and, by IC's reckoning, it is now the largest construction equipment manufacturer in China. This is mainly thanks to its acquisition of crane builder Puyuan at the start of 2004, making 2005 the first full financial year of trading for the company following the merger.

The general slide of Chinese manufacturers down the Yellow Table seems to be related to the credit squeeze that the Central Government instigated in mid-2004. It clearly had the desired effect of 'gently pressing the brakes' on China's overheating economy and the result seems more pronounced last year than in 2004.

This is because 2004 was a mixture of high sales at the start of the year, followed by seven months of post-squeeze conditions, which clearly averaged-out at a reasonable level. In 2005 however, the entire year was spent in these post-squeeze conditions, with the sales growth seen as the year drew to a close not quite bringing things back to 2004's overall volume.

Outlook

It is always dangerous to make predictions, but it seems likely that this year will see a resurgence for the Asian manufacturers. The Japanese economy is picking up, and despite 2004's credit squeeze, demand for construction equipment in China is growing again.

Overall growth in the industry clearly slowed in 2005, and it remains to be seen whether 2006 will be another year of increased sales. Any growth there is will probably be small, and much depends on what happens in the US, and to a lesser extent, European markets. They could both shrink this year, and if this does happen, the industry will hope that any losses are offset by stronger conditions in Asia.

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

CONNECT WITH THE TEAM